European plastics industry braces for increased instability, higher prices, and lower growth

European plastics industry braces for increased instability, higher prices, and lower growth

The European plastics industry is tackling challenges on multiple fronts. In packaging, by far its biggest market, it has become a victim of its own success, particularly as the ideal material for single-use applications and people on the move.

In building and construction, some infrastructure projects may go on hold as governments divert some funds away from infrastructure projects to defence, although business is being boosted as consumers get help to improve energy efficiency in their houses. In automotive, component suppliers are suffering because car makers have been cutting production – not as a reaction to reduced demand, but because they cannot obtain the chips they need for their electronics.

Since early 2019, COVID-19 has had major effects on production, occasionally positive but mostly negative. And now, just as Europe and the rest of the world was recovering from the devastating two years of the pandemic, we have the tragedy of the Ukraine conflict.

Discussing the situation in late March, Martin Wiesweg, Executive Director Polymers EMEA at consultant IHS Markit, said that, quite apart from causing a humanitarian disaster, the crisis is weighing heavy on the plastics business, in terms of cost inflation, the worsening of supply chain bottlenecks, including energy supply, while also raising the spectre of demand shock amid the fear of global stagflation.

Inflation across the EU hit an all-time high of 7.5% in March. S&P Global Economics said on March 30 that it expects eurozone growth to be 3.3% this year, compared to 4.4% in a previous forecast, and inflation to reach 5% this year and stay above 2% in 2023.

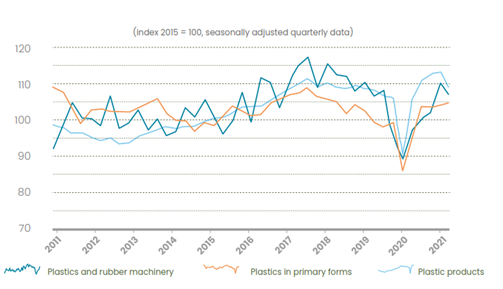

“In the past, high crude oil prices weighed negatively on European plastic demand (see chart) ,” says Wiesweg. Prices soaring further could see consumer disposable income slumping, impacting retail sales. Sectors driven by consumer discretionary income like white goods, consumer products, and automotive would fare poorly as buyers try to conserve cash. “In the short to medium term, Europe could potentially see a demand contraction across polymers.”

Plastics processing is on course for the circular economy

Germany remains the powerhouse of the European plastics industry, with its multiple strengths in materials, equipment, and processing capability. But some sectors are hurting all the same. According to German plastics processing industry umbrella organisation GKV, industry sales increased by 12.6% to €69.4 billion in 2021, but member companies remain under a lot of pressure to produce good results. It cites “exorbitant cost explosions” for raw materials and energy, as well as the many delivery delays and resulting order suspensions, particularly in automotive supplies.

The automotive sector has provided a unique set of problems. Several European car makers have temporarily shut down production in recent months, with important negative effects in the supply chain, including the permanent closure at some processors. Passenger car registrations fell by 2.4% in 2021 to just below 10m units across the 27-country EU, according to the European Automobile Manufacturers Association, ACEA. Jincy Varghese, demand analyst at ICIS, forecasts EU automotive output to grow 17% in 2022, although it will still be down 26% from 2019 levels. A healthy recovery is only likely in the second half, she said in February.

The overall economic outlook for 2022 remains very mixed, said GKV president Roland Roth at the association’s annual results conference in early March. Around half of association members expected sales growth when poled in the run-up to the conference, but a good quarter expected further falls. Several were thinking about relocating or terminating production.

Roth called for a reduction in government surcharges on energy prices. As for material prices, he said recent increases have been “almost insane.” On average, prices for plastics in Europe increased by more than 50% year-on-year in the first half of 2021 and have stayed high. In February 2021, for example, virgin PET sold for around €1/kg. In March of this year, the price was around €1.7/k. Linear low density PE went from around €1.2/kg to around €1.9 over the same period.

But the GKV President remains optimistic: "In 2022, as plastics processors, we will continue to get the best out of polymer materials and successfully complete the tasks ahead,” he said.

Alarm bells have been ringing over energy prices at Unionplast, which represents Italian plastics processing companies. "The crisis in energy prices is seriously affecting a sector that has over 5,000 companies, and more than 100,000 employees," says Marco Bergaglio, President of the association.

"The uncontrolled increase in energy costs and the growing difficulty in finding raw materials is a deadly mix for our sector and creates the real risk of not being able to meet the demands of our customers. This situation has inevitable consequences also on the prices of our products.”

European machinery makers in good shape

The picture is brighter with European plastics equipment suppliers. Thorsten Kühmann, Secretary General of EUROMAP, Europe's Association for plastics and rubber machinery manufacturers, said in March that member companies' order books were “filled to the brim. The current year will therefore be another very good year. We expect sales to increase by 5 to 10%.” However, here too, rising prices and now the war in Ukraine are increasing uncertainty.

Dario Previero is president of Amaplast, the association of Italian producers of plastics and rubber machinery and moulds. At the end of last year, he said: “According to our estimates, at the close of 2021 production should be a hair’s breadth from pre-pandemic levels, up 11.5% with respect to 2020. The clear recovery recorded in 2021 gives us good reason to expect performance beyond pre-crisis levels in 2022.”

Ulrich Reifenhäuser, CSO of Reifenhäuser Group and also chair of the K exhibitor advisory board, says the company has “an extraordinarily positive” order backlog for the current year. “A major factor here was the extremely high demand for our melt-blown nonwovens lines, which have made a decisive contribution worldwide to being able to produce sufficient medical protective masks to combat the pandemic - especially in Europe with local production capacities.”

Looking back at the financial year that has just closed for injection moulding technology major Engel, CEO Stefan Engleder said in mid-March: “We are closing a year with great challenges, but also great opportunities. We will close the 2021/2022 business year with a significant increase over the previous year. Material bottlenecks are currently one of the major challenges. So far, we have managed to avoid delivery delays as far as possible.”

Gerd Liebig, CEO of another injection technology major, Sumitomo (SHI) Demag, says that overall, consumption figures are good. “Nevertheless, the coronavirus situation clearly had an impact on demand. But we are anticipating a fast recovery due to our strength in business strategy.” Sales of machines are on track to surpass pre-pandemic levels at this company too.

“Demand continues to increase for all-electric models, and we anticipate this ratio will continue to increase,” says Liebig. “We’re forecasting further increases in 2022 in the automotive and consumer sectors. A decade ago, 20% of our machines were fully electric; now it is more than 80%.”

Packaging challenges

High and escalating resin prices globally means the packaging market is under continuing pressure, says Liebig. “Given that recyclable granular is now at the same price as virgin polymer was 12 months ago, the impetus to lightweight now stretches across all packaging material substrates, not just virgin polymers. We continue to focus on reducing material usage by improving the process and enabling our customers to produce ever thinner-walled parts.”

The move towards tethered caps (mandatory from 2024 under Single-Use Plastics Directive, or SUPD) and extensions of Extended Producer Responsibility (effective 2023) will inevitably have a strong influence, as does the new EU Packaging Levy on non-recycled packaging waste, Liebig says. (Since Jan 1, 2021, the EU charges member states €0.80/kg of plastics packaging waste that is not recycled. States are free to choose how to finance the levy.)

The European plastics industry is in fact having to contend with various pieces of legislation relating to plastics waste. For example, there is now a mandate that 55% of all plastic packaging in the EU be recyclable by 2030, as well as the levy on non-recycled plastic packaging waste. Some countries are also introducing local legislation (Spain and France for example), making the playing field not as level as it should be.

Industry is already having to face up to some consequences of the SUPD, some elements of which came into force on 3 July 2021 in most EU countries – although the roll-out of the legislation has not been entirely smooth. In Italy, for example, it only became law in January, with a delay on final implementation; it is also more flexible in its definitions of plastics products than Brussels originally intended, and whereas the SUP Directive does not exempt certain biodegradable plastics, the Italian legislation does.

On the subject of bioplastics, the European Bioplastics trade association says: “Unfortunately, in Europe, bioplastics still don’t obtain the same degree of support that other innovative industries receive from EU political decision makers. The EU Commission has sometimes contradictory positions on bioplastics. Member State positions on bioplastics also vary a lot, the regulatory environment is anything but harmonized.” This discourages investment in R&D and in production capacities, it says.

Despite these challenges, development in European bioplastics is “very positive. Global production capacities still represent less than 1% of the more than 367 million tonnes of all plastics, but by 2026, bioplastics production will pass the 2% mark for the first time.” Production capacities for bioplastics in Europe were close to 600,000 tonnes in 2021 and can be expected to increase to around 1,000,000 tonnes within the next five years.

In the UK, now outside the EU, a new tax on plastic packaging came into force on April 1 of this year. The tax will apply to plastic packaging components that do not contain at least 30% recycled plastic and that are either manufactured in the UK or imported into the UK (again, there are exemptions). The tax will be levied at a rate of £200/tonne (approx. €235/tonne).

At the British Plastics Federation, Director-General Philip Law is determined to see the positive side. “The Plastics Packaging Tax could ultimately be a platform for innovation and help reduce the heat of public debate,” he says.

Recycling on the rise

“New legislation and targets for the recycling of plastics and the use of recyclate are changing the way the whole plastics industry must operate,” says Elizabeth Carroll, Consultant, Recycling and Sustainability, at AMI Consulting in Bristol, UK, which has a new report out on mechanical recycling in Europe. “The mechanical plastics recycling industry, therefore, has become the focal point for investments, acquisition, and expansion,” she says.

Plastics recyclate production in Europe was 8.2 million tonnes in 2021 and is forecast to grow at a rate of 5.6%/year to 2030. That compares with the 35.6 million tonnes of commodity plastics that entered the waste stream in 2021. “This implies that Europe achieved an overall plastic recycling rate of 23.1%,” says Carroll. That figure is most likely to rise as the plastics industry makes major investments in recycling technologies of diverse types.

The picture of how to convert recycled plastics into high-value products is brightening. Says Engel’s Engleder: “Thanks to horizontal networking along the value chain, we will no longer have to downcycle materials in the future, but can actually re- or even upcycle them. If we exchange information and data across companies, we will be able to recycle plastic waste and produce high-quality plastic products from it again. Digital transformation is the prerequisite for rapidly advancing the issues of sustainability.”

At Sumitomo (SHI) Demag, CEO Liebig agrees that recyclate processing in itself is not an insurmountable technological challenge. “The greatest challenge is achieving comparable component performance and stabilising non-uniform material properties through intelligent process monitoring,” he says. “There are many promising projects underway, although recyclate performance is still dependent on purity.”

Michael Ruf, CEO of KraussMaffei, which has injection and extrusion technologies under its belt, says: “Circular Economy is not only an ecological but also an economic imperative. It is therefore a supporting pillar of KraussMaffei's product strategy. Customers have already recycled more than one million tons of plastics with our systems.”

And at compounding equipment company Coperion, Marina Matta, Team Leader Process Technology Engineering Plastics, says: “We are observing many ground-breaking developments that significantly improve the sorting and washing quality of waste. The pyrolysis process has also recently been significantly enhanced so that this recycling process can be carried out in a much more energy-efficient way.”

Polymer suppliers going green

European polymer producers are making major efforts to improve the sustainability of their products. At polyolefins and compounds major LyondellBasell, Richard Roudeix, Senior Vice President - Olefins & Polyolefins Europe, Middle East, Africa and India, says: “Becoming climate neutral by 2050 requires the industry to go through a deep transformation in a relatively short time frame, especially considering that some technologies to completely decarbonise our processes are still in early phases of development. Currently, high costs for energy are compressing industry profits at the exact moment the industry needs additional funds to make decarbonization investments.”

Polymer suppliers have not been entirely eye to eye with European policy makers on how to move to a green economy, but opinions are converging. “LyondellBasell believes alternative government policies and voluntary measures are more effective than relying uniquely on national taxes in achieving environmental goals,” says Roudeix. He suggests that a fee based on a product’s recyclability could be used to fund improvements in plastics recycling infrastructure and programs.

LyondellBasell aims to produce and market two million metric tonnes of recycled and renewable-based polymers annually by 2030. It has already launched plastics made from mechanically and chemically recycled plastic waste, as well as bio-based feedstocks.

Similar comments come from SABIC. In 2019, it launched certified circular polymers produced by upcycling used plastics. “However, the reality is that there is currently greater demand for recycled plastics than the supply available,” says a representative. “Manufacturers need to find a way to scale up in order to instigate real change.”

Greater regulatory support from governments is required to help industry players scale new techniques such as chemical recycling, says SABIC. “For example, it is important that the European regulatory framework recognize chemical recycled resin as equivalent to virgin resin produced from fossil feedstock in order to increase availability and drive scalability.”

At BASF, which like SABIC has a broad pallet of plastics aimed at multiple markets, a representative says: “We expect that plastics will play a vital role in achieving the EU´s net zero emissions goals by helping to deliver emission savings for key sectors like construction, automotive, or food packaging. We are striving worldwide to achieve net zero CO2 emissions by 2050. In addition, we want to reduce our greenhouse gas emissions worldwide by 25% by 2030 compared with 2018.”

Polycarbonate and polyurethanes major Covestro has one of the boldest strategies among polymer suppliers. Its target is to have net zero emissions for scope 1 and 2 (related to its own production and external energy sources) by 2035.

Plastics Europe Managing Director Virginia Janssens, Managing Director, Plastics Europe, says its members support the 30% EU mandatory target for recycled content in plastics packaging by 2030 and have recently announced 7.2 billion euros of planned investments in chemical recycling by 2030 in Europe.

Throughout and beyond what hopefully will be the temporary crises of COVID and Ukraine, “the world remains firmly focused on circularity, plastic pollution, and environmental leakage,” says Wiesweg at IHS Markit. “The circularity drive will spur innovation in chemical recycling, helping achieve world scale commercial viability which along with mechanical recycling will steadily displace virgin plastic resin.”

K 2022 - the world's most important trade fair for the industry

In 2022, as every three years, K in Düsseldorf will once again be the most important information and business platform for the global plastics and rubber industry. Nowhere is the internationality as high as in Düsseldorf. Exhibitors and visitors from all over the world will come together and take advantage of the opportunities from 19 to 26 October this year not only to demonstrate the industry's capabilities and present innovations, but also to exchange views on the situation of the plastics and rubber industry in the various regions of the world, discuss current trends and jointly set the course for the future.

www.k-online.com